Black Scholes Model

On most trading desks today, the Black–Scholes formula is like Latin: it is no longer used in its original form, yet modern trading practices are built upon it. This Nobel Prize-winning formula once offered a simple mathematical approach to option pricing. However, in current markets, it serves primarily as a reference framework and benchmark rather than as a direct tool for executing trades. In this essay, we will examine the formula in depth: how it operated, its original applications, and the reasons it is no longer viable without significant modifications. Let us start from the basics. An option, in simple terms, is a contract that gives you the right, but not the obligation, to buy or sell a stock at a fixed price at or before a set date. There are two kinds of option styles- American and European. The main difference is that American-style options can be exercised before expiration, whereas European-style options can only be exercised at expiration. You probably know this already, but it is worth restating because the Black Scholes formula applies only to European-style options.

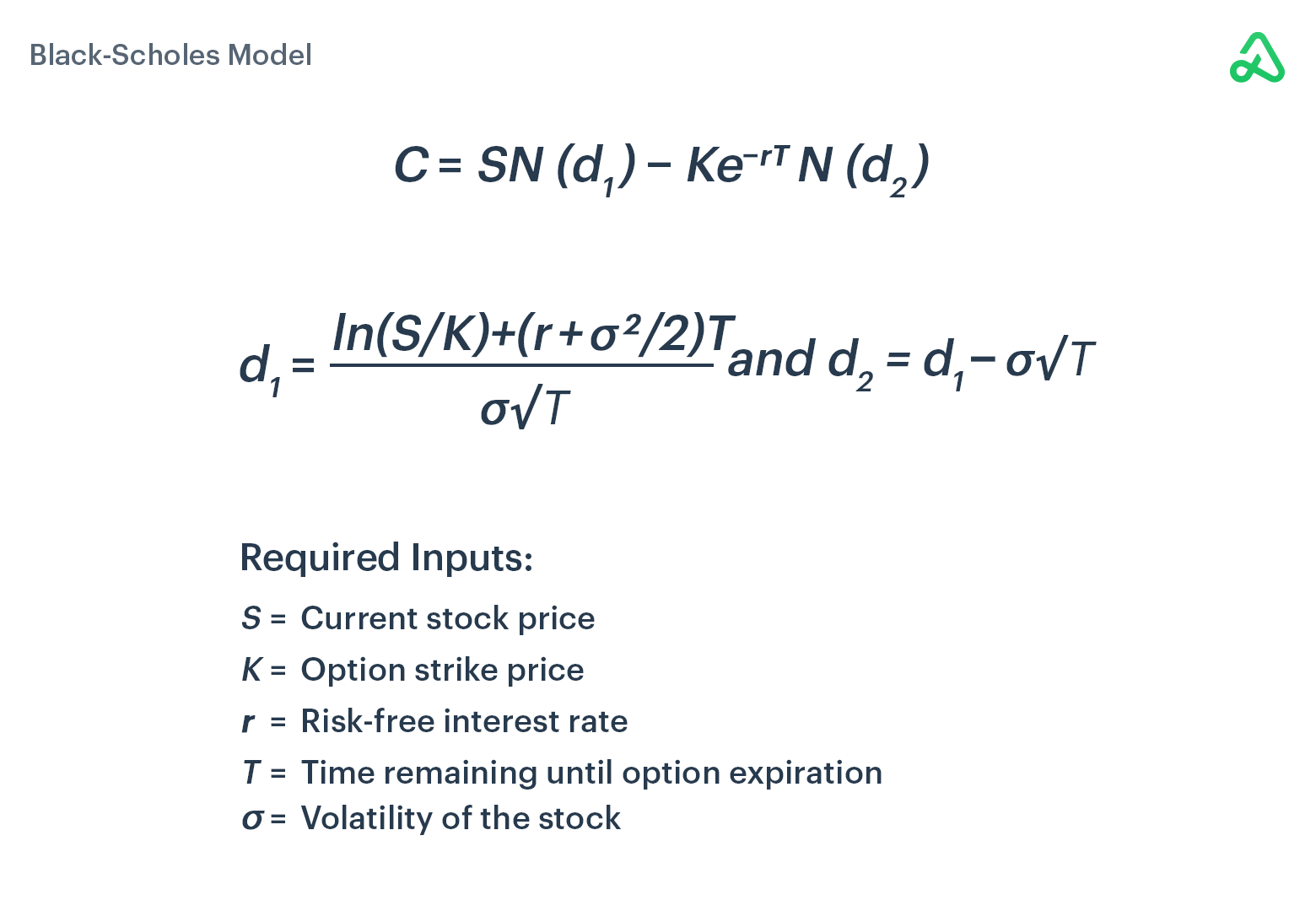

Let us take a look at the actual formula:

Now this seems very complicated and abstract, but at the end of the day, there is a simple way to understand this formula. The Black Scholes formula takes five inputs: the current stock price, the strike price, the time to expiration, the risk-free interest rate, and the volatility of the stock. Under its assumptions, the stock price is modeled as a random process that can move up or down over time. By plugging those five inputs into this stochastic framework, the formula produces one single output: the theoretical fair value of a European option on that stock. At the time, it was groundbreaking. For the first time, traders could make decisions about an option position mathematically. This formula basically told investors whether the option was over or undervalued. Based on this, just as we would today, if it was overvalued, you would go short, and if under, you would go long. This insight earned Scholes and Merton the 1997 Nobel Prize in Economic Sciences and cemented the model’s place in financial history. In the early days, trading desks actually used it by plugging in the numbers, getting a price, and making a trade.

But markets change, and Black-Scholes has not aged perfectly. The formula relies on several big assumptions, for example, that volatility remains constant throughout the option's life and that prices move smoothly without sudden jumps. That setup made sense on paper back in 1973. But very obviously, in the real world, it doesn’t hold. The most significant event that showed the unreliability of Black Sholes formula was the 1987 Black Monday crash, when the S&P 500 tanked 20% in one day, and volatility shot up unevenly across options. It showed that a model which was idealistic cannot hold up in an ‘un-ideal’ world. However, this did not mean that the formula was useless or immediately thrown out.

Today, most traders don't use the raw formula. They make some modifications. For example, they layer on models like the Heston model, where volatility itself moves randomly, allowing for more realistic predictions. Secondly, some traders layer Jump-diffusion models, like the Merton Jump-Diffusion model, to predict stock prices when they suddenly jump. Overall, even though no one relies solely on the formula anymore, its structure still lies at the foundation of modern quant trading. Every advanced model, from stochastic volatility to jump-diffusion, starts with Black-Scholes as its base. It is outdated in practice but essential in philosophy, forming the backbone of how we quote, hedge, and understand options today.